How To Value a Startup?

WeWork’s shambolic IPO endeavor has started a considerable number of intriguing peruses: everything about the organization has been covered, from the whimsical propensities for the originator and previous CEO Adam Neumann, his land dealings, just as the ramifications for its principle benefactor, Softbank, and the eventual fate of the organization, which actually needs cash, regardless of whether the IPO fizzled.

Other than the entrancing unfurling and the fun at others’ expense, in any case, a few inquiries that have been represented that have a lot of suggestions and weight are around the valuation: how should the valuation be so “wrong”? For what reason did this occur? How might the current high valuations affect financial backers and new businesses?

While these are altogether unquestionably fascinating conversation focuses, a more principal question calls, and one to which there is not really an obvious response: how can one esteem a startup or a scaleup? What is the right startup valuation model? Especially for one that doesn’t cause incomes to yet and for which there is no unmistakable course of events for doing as such?

This is an inquiry that plagues the two originators—when they are raising assets for their organization, and financial backers, who have a premium in valuations heading the correct way both at the hour of their venture and their exit. Be that as it may, showing up at a figure everything gatherings can concur upon isn’t exceptionally clear; at last, valuation is a greater amount of craftsmanship than a science.

In this article, we will recap customary valuation techniques just as probably the most regularly involved strategies for new businesses, and give some helpful rules and best practices.

Conventional Valuation Methods – Brief Recap

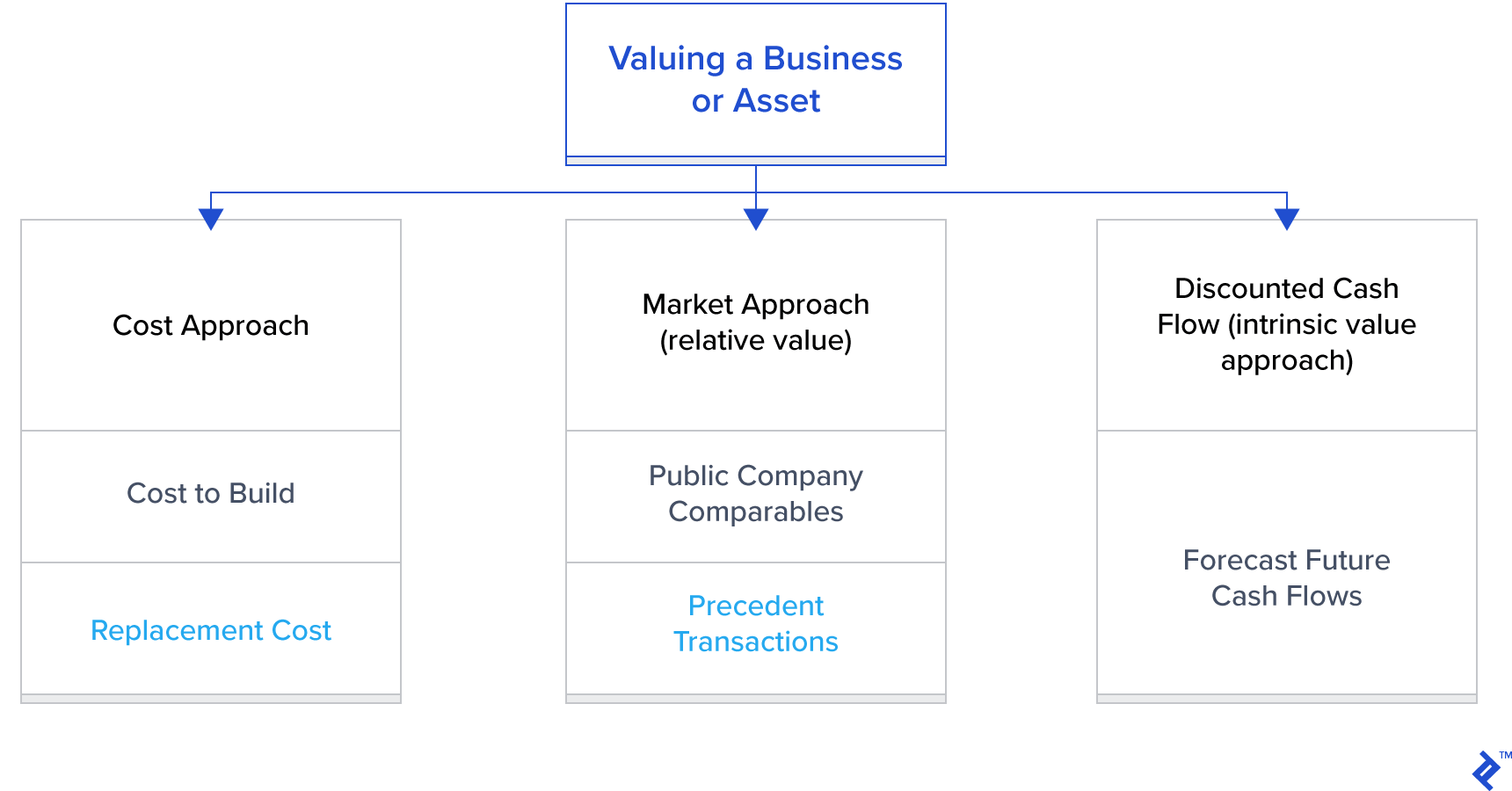

Contingent upon the motivation behind the valuation practice and the express the organization is in, it tends to be esteemed as either a going concern, an organization that will keep exchanging, or a gone concern, a business that is being slowed down or sold. In the last option case, the future benefit is unessential (for clear reasons), and the valuation will zero in on what is recoverable from the offer of the organization’s resources. This is past the extent of this article. For an organization that is relied upon to keep exchanging for years to come, there are viably three fundamental methods of valuation:

Cost approach: This valuation method is viably a gone concern valuation. The valuer takes a gander at the expense (subsequently the market worth) of every resource of the organization and disregards pay. It can likewise be utilized to ascertain the base worth of the organization, a kind of a valuation “floor.” For this explanation, this method is seldom utilized outside of the land.

Market approach: This is the speediest and most instinctive method of doing a valuation. It is fundamentally a relative valuation: the thought is that comparative organizations ought to have a comparative worth. The professional hence distinguishes equivalent organizations by taking a gander at either securities exchange information or exchanges (private or public). Most generally, these valuations are finished by taking a critical monetary measurement (like profit or EBITDA) and afterward applying a pertinent numerous to it. The numerous is typically gotten from noticing exchanges in comparable organizations. The exactness of a valuation of this kind clearly relies upon the number of information focuses that can be extrapolated and the number of comparative organizations exists that have gone through exchanges.

Pay approach: This is the most exhaustive technique for esteeming an organization. Future incomes are projected throughout some stretch of time with the end goal that they can in any case sensibly be assessed. The not-not-so-distant future is assessed through a terminal worth. The incomes are then limited to the present using a suitable rate. The outcome is the natural worth of the business—what it is worth as an independent substance and in view of its money-creating potential. The primary test here, obviously, is precisely anticipating incomes, ones that are made through sensible and proficient suppositions.

Business Valuation Methods

Valuation for Startups: A Philosophy

Yet, what techniques are generally exact to esteem a startup? The strategies portrayed above plainly represent a few challenges when taking a gander at beginning phase organizations. For instance, how should the expense approach be applied to an organization that holds not very many resources outside of immaterial resources, like the group’s capabilities and the legitimacy of the thought? Or then again how could an income numerous be applied to an organization that doesn’t yet have incomes? Therefore, after some time, the beginning phase of organization valuation has arisen as a different field in corporate money.

There are likewise strains among financial backers and business visionaries, as the previous have every one of the motivators to keep valuations lower, while business people need to see their endeavors compensated through an appealing valuation.

So how might one consider startup valuations? At last, the “right” valuation is the one that gives business people the assets they need to arrive at the organization’s achievements for the stage that they are in. It likewise gives them an opportunity to commit themselves to the business without continually zeroing in on gathering pledges. Simultaneously, it doesn’t offer such a part of the organization that could risk their command over it through the weakening of resulting adjusts. The rationale is reflected for financial backers: they should mean to obtain an adequate stake in the organization that permits them to have some control, while as yet having arrangement and “dog in the fight” from business visionaries. It is likewise vital that the valuation isn’t excessively hopeful to stay away from a down round. Hence, financial backers should be clear about: a) what should be accomplished as far as items and deals before the organization needs another capital infusion; and b) why a more fruitful and educated financial backer is more helpful to a business person than somebody who will simply contribute cash.

The construction of the speculation likewise matters: adventure financial backers usually use “drawback security”— most frequently as a convertible note or a liquidation inclination. This is made fundamental by the exceptionally dangerous nature of the beginning phase contributing. Fred Wilson clarifies this obviously through what he calls the 1/3 rule:

“1/3 of the arrangements truly work out the manner in which you figured they would and produce incredible increases. These additions are frequently in the 5-10x territory. The business people for the most part excel on these arrangements.

1/3 of the arrangements wind up going for the most part sideways. They transform into organizations, yet not organizations that can deliver critical increases. The additions on these arrangements are in the scope of 1-2x, and the financial speculators get most to all of the cash produced in these arrangements.

1/3 of the arrangements end up being terrible. They are closed down or sold for not exactly the cash contributed. In these arrangements, the financial speculators get all the cash despite the fact that it isn’t a lot.

So assuming you take the 1/3 rule and add to it the run-of-the-mill construction of a funding bargain, you’ll rapidly see that the financial speculator isn’t actually arranging a worth by any stretch of the imagination. We are haggling the amount of the potential gain we are going to in the 1/3 of our arrangements that really produce genuine additions. Our arrangement structure gives the greater part of the disadvantage assurance that ensures our capital.”

Eventually, these three focuses are what makes a difference while arranging the provisions of a beginning phase venture:

How much cash does the organization have to arrive at the achievements set before they next need to raise reserves?

What is the best capital design to adjust the interests of business visionaries, financial backers, and at last workers?

How much is the marketable to pay for a stake in an organization like mine?

An obsession with the feature number of the valuation can be on occasion harming business visionaries.

Beginning phase Company Valuation: Methodologies

Given these standards, what is then the best procedure to utilize while esteeming a beginning phase organization? We take a gander at three of the most widely recognized techniques utilized by private backers and VC.

Scorecard or Checklist Method

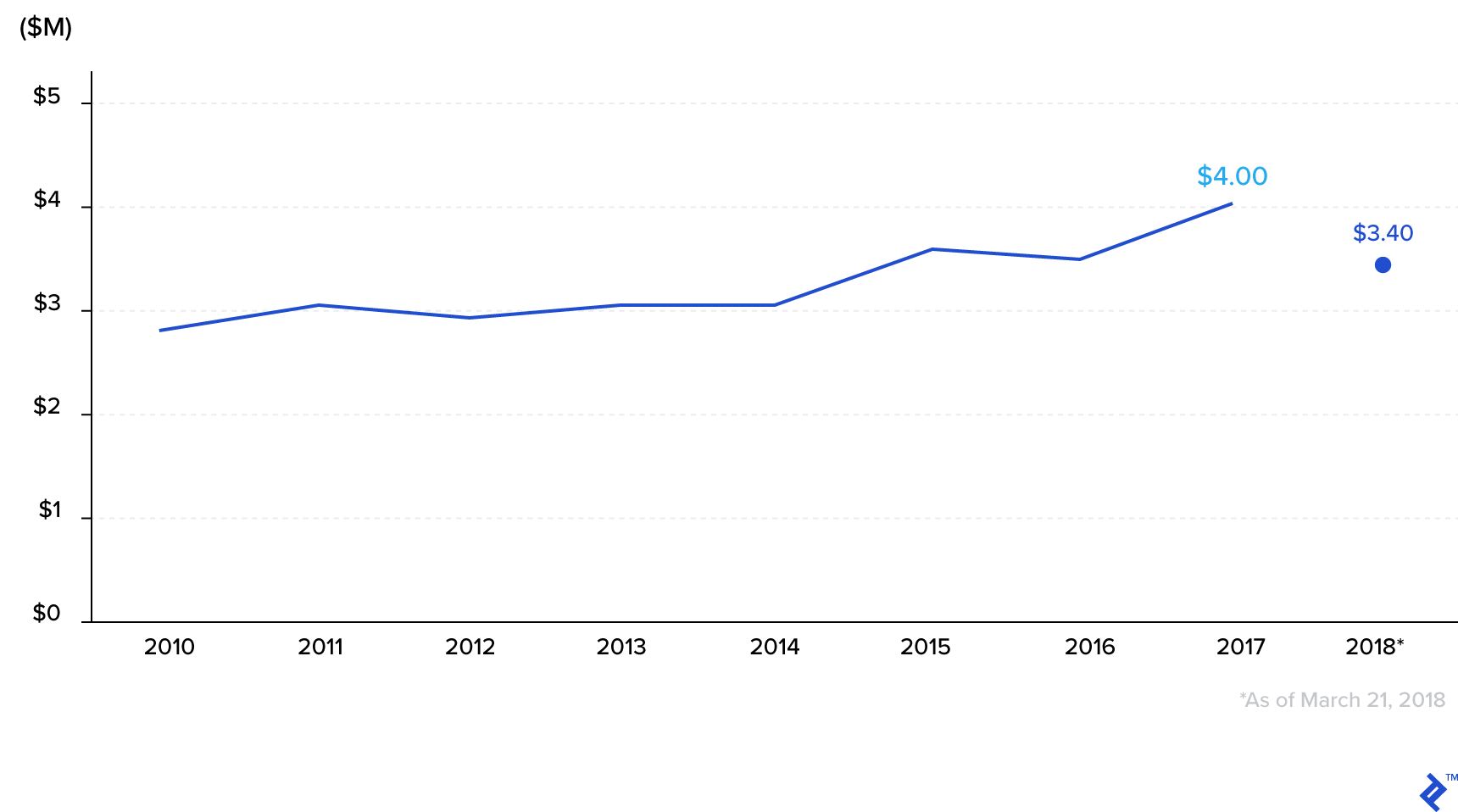

The scorecard strategy was portrayed by Bill Payne and formalized in his manual on the most proficient method to fund-raise from private backers. The financial backer should initially take a gander at the normal valuation for organizations at a comparable stage and in a comparative industry to the one they are assessing and track down a normal valuation For organizations looking for holy messenger financing, this worth has gradually been crawling up over the long haul, with an expected normal worth of $3.4 million of every 2018.

When the normal has been set up, the financial backer will then, at that point, apply a multiplier, in light of their appraisal of the accompanying subjective variables and the weight they choose to apply to them inside the set reach.

The strength of the Management Team (0–30%)

Size of the Opportunity (0–25%)

Item/Technology (0–15%)

Cutthroat Environment (0–10%)

Promoting/Sales Channels/Partnerships (0–10%)

Need for Additional Investment (0–5%)

Other (0–5%)

The multiplier will then, at that point, be 1 for a normal organization, or lower/higher for an organization that is more terrible/better than the normal. Clearly, the aftereffects of such a valuation are exceptionally reliant upon the closely held individual belief of the heavenly messenger and on their mastery and experience. A very much like the strategy is the agenda technique, created by Dave Berkus, which allows fixed loads to each characterized class.

DCF with Multiples

Similar to a standard DCF, this depends on monetary projections made by the startup supervisory group. To compute the terminal worth, the last projected EBITDA (or comparable figure) is then duplicated by the numerous extrapolated from a gathering of comparables. The incomes are then limited utilizing a rate that addresses the weighted expense of assets (obligation and value). There are two significant difficulties with such a strategy. In the first place, the projections are destined to be erroneous; second, it is amazingly difficult to decide the fitting rebate rate to be applied. This web article offers a few rules.

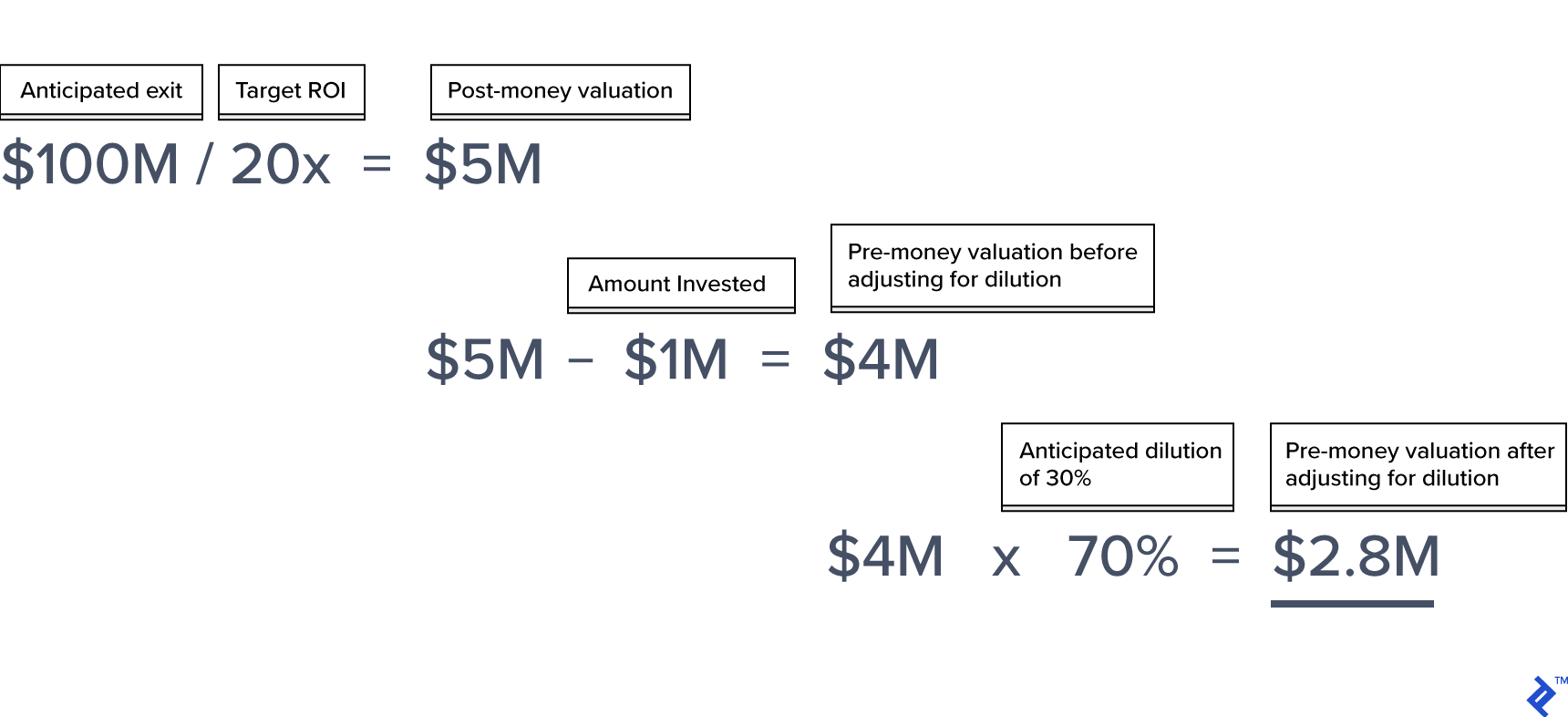

Investment

This is an industry-standard strategy that considers the necessary return pace of the asset and their speculation skyline. Essentially, it requires ascertaining post-cash valuation (of the current round)— in light of the expected leave sum and the objective return of the asset—and afterward changing by ticket size and expected weakening. The fundamental shortcoming of this technique is that it centers just around the suppositions of the endeavor financial backer, not on the organization’s qualities.

Achievements for Each Round

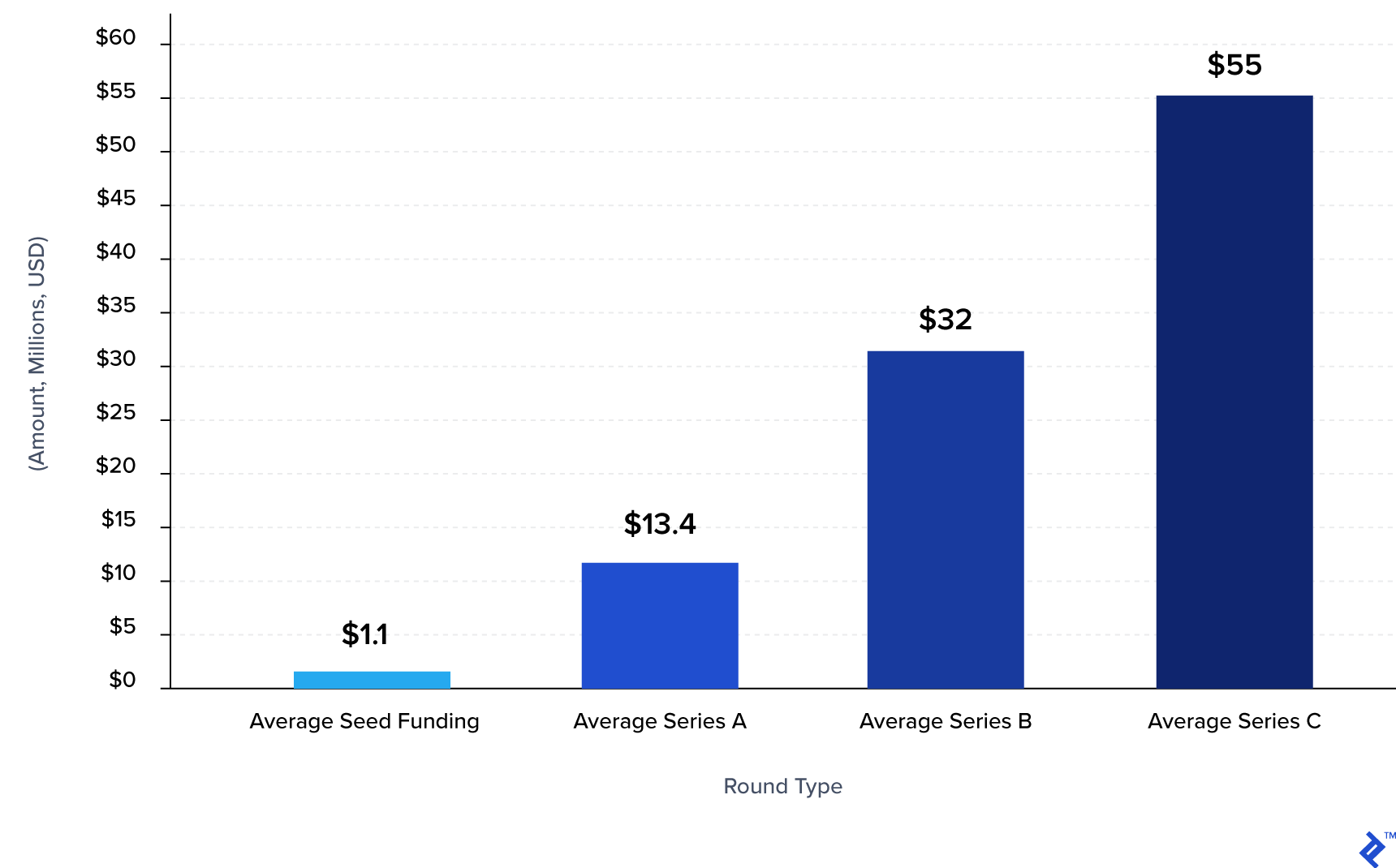

At long last, it merits examining the normal valuations and achievements for each subsidizing round. This article gives a far-reaching clarification of the various phases of financing for an organization and the size of the individual valuation round. It is essential to remember that round sizes and valuations are a lot more modest outside of the US, and surprisingly in the US outside of Silicon Valley.

Beginning stage: this is the domain of private backers – the most hazardous phase of any organization. Now, the organization is truly thought and a little, devoted group.

Loved ones: The startup is subsidized either by the actual authors or through the assistance of assets and family members. This furnishes the organization with the main assets to chip away at the thought; contributed sums are typically under $250k, valuation $1 million.

Heavenly messenger/Seed: The principal outer financing comes to the organization, and will ordinarily have a model at this stage – the organization puts resources into colleagues and promoting. The speculation got is for the most part around $500k/750k, for a valuation of ~$2/4 million.

Seed: Not generally a different round. The principal proficient financial backers come ready, anticipating a push on client procurement.

Development stage: this is the common investment jungle gym. Organizations are attempting to track down item market fit and afterward scale.

Series A financing: Typically, at this stage, the organization has sent off an item and is chipping away at making it fruitful, with item and plan of action changes. Series A rounds might back $2-$5 million.

Series B financing: This round serves to additionally demonstrate the model tried during Series A – the assets raised will go to test the development switches, work on the item, and professionalize the group. Series B will be around $5-$15 million.

Series C + subsidizing: At this stage, the organization has a clear item/market fit and is simply contributing to speed up development. However, it might possibly be producing income. Series C rounds will be $15+ million and each ensuing round size will increment appropriately.

End

Eventually, it is critical to recall that for a startup, or a beginning phase organization, the valuation isn’t put together such a great amount with respect to the current (or future, as the chances of the organization making it are so low and difficult to foresee) as on immaterial factors like the strength of the thought, the abilities of the group, and the business it works in. It is significant for business people not to get focused on high startup valuations, which might be difficult to maintain. The objective of a top-notch subsidizing round is that of giving the organization adequate runway to meet its achievements while guaranteeing that the motivations are adjusted for all partners.

{kind=link}