What Is a Leveraged Buyout?

Matt Levine of Bloomberg characterizes LBOs conveniently: “You acquire a truckload of cash to purchase an organization, and afterward you attempt to work the organization such that brings insufficient cash to take care of the obligation and make you rich. Once in a while, this works and everybody is glad. Once in a while, it doesn’t work and at minimum certain individuals are dismal.”

Adequately straightforward?

Wikipedia has a more specialized view: “A utilized buyout is a monetary exchange wherein an organization is bought with a blend of value and obligation, to such an extent that the organization’s income is the insurance used to get and reimburse the acquired cash. The utilization of obligation, which typically has a lower cost of capital than value, serves to decrease the general expense of financing the securing. The expense of obligation is lower since interest installments frequently decrease corporate personal assessment risk, while profit installments typically don’t. This diminished expense of financing permits more noteworthy additions to gather to the value, and, thus, the obligation fills in as a switch to build the profits to the value.”

This definition might be precise, yet who can get by on such an extra supper?

My own view is that an LBO is one of the numerous decisions at the nexus of how to utilize investable money and how to fund an organization. In specific circumstances, an LBO can be an amazing decision on the two counts. In different cases, not really. In this article, I will diagram a portion of the reasons an LBO may be sought after, why it very well may be unique in relation to different decisions that exist to put resources into the value of an organization, and the stray pieces of demonstrating an expected arrangement.

The Five Ways to Make Money as an LBO Investor

Truly, there are just five methods for bringing in cash as an LBO financial backer, or truly as a financial backer overall:

Resource improvement – which we can part into:

Income development

Cost decrease

Monetary designing

Market timing

Market beta

That is it. Assuming you can’t think that it is in one of those classes, then, at that point, it’s not there. There are likewise contentions to be made for or against every one of these things (I have genuine reservations, for instance, that market timing is a practical pathway). Yet, various financial backers have various assessments and carry diverse mastery to their speculations, and another financial backer may view that pathway as a feasible procedure.

Utilized buyouts are intriguing in that they can play on these components, with specific exchanges depending more on either as the basic reasoning for the speculation postulation.

Income Growth

Methodologies depending on income development include purchasing an organization and developing its income at a comparable cost proportion, bringing about an improvement of its profit before interest, duties, devaluation, and amortization—or EBITDA—and afterward renegotiating or selling it at the equivalent various (however on a higher EBITDA base).

Cost Reduction

These systems depend on the execution of cost-cutting projects. Like the income development model, the progressions made mean to further develop EBITDA, at last prompting a renegotiate or deal at the equivalent various (yet on a higher EBITDA base).

Monetary Engineering

Here and there, the characterizing component of an LBO is the idea of changing an organization’s expense of capital by executing an alternate monetary construction, regardless of whether the organization’s activities (as far as incomes and costs) change or not. Three instances of monetary designing techniques are:

Diminish an organization’s weighted normal expense of capital by causing a bigger measure of obligation (or other more effective capital) than exists before procurement, bringing about a better return to value.

Re-figure an organization’s resources to bring down its capital expenses by means of pseudo-financing exchanges. For instance, through the deal leaseback of organization genuine properties or capital resources, deal and permitting of key protected innovation, figuring of different resources the organization might control, or the execution of more forceful working capital plans.

Consolidate an organization with different organizations or resources that the financial backer possesses, expanding its scale so the market will actually want to pay a higher numerous for the joined organization: Known as a roll-up system, this is a regularly involved technique in the retail area—for instance, where one can frequently purchase establishments at a lower various as single stores and sell them for a higher various later a specific minimum amount has been accomplished as far as a number of stores held by the association.

Market Timing

An organization is purchased with the conviction that the value various at which it is evaluated will improve and set out the freedom for a renegotiate/deal at preferred terms over exist in the current market.

While this procedure should be referenced and, at last, changes in market value assumptions play into all speculations of any sort, in my experience, I presently can’t seem to observe any financial backer that can dependably anticipate market value changes throughout extensive stretches of time. (Assuming that is you, kindly connect—I might want to contribute.)

Market Beta

The market beta system is like market timing in that the financial backer executing the methodology is depending on market influences—rather than changes at the resource level—to drive returns. The distinction, however, is that the market beta financial backer is skeptical about an organization’s development prospects and changes in market estimating, yet rather has the attitude that openness to the market throughout significant stretches of time has generally conveyed income. The market beta financial backer has the point of view a greater amount of a record reserve financial backer, attempting to enhance ventures and depending on the drawn-out development of resources overall to convey profit.

A common LBO exchange might incorporate a blend of numerous or even these elements in shifting degrees, and it’s valuable to ask while assessing a likely venture, “Which of these things am I depending on for my profits?” While it is just episodic, in my experience, the initial three components are considerably more controllable than the last two, and an arrangement that includes timing the market or simply being in the game rarely brings about alpha returns.

Charge Shields and Loan Covenants

While most of the techniques to prevail in an LBO obtaining are genuinely clear (reasonably, if possibly not essentially), there are different angles that are not exactly as direct. One of the most significant of these, as I would see it, is the improperly named charge safeguard. While I would rather avoid the term, I myself will involve it in the remainder of this article since it is successfully universal in LBOs. I would unequivocally incline toward the term to be the more unmistakably named charge move, or expense redistribution, both of which would all the more obviously underline the genuine elements of this component.

The hidden idea of assessment safeguards is that in most cases, a partnership should pay charges on its benefits (which eventually have a place with the organization’s value holders), yet not on interest paid to a moneylender, which is viewed as a cost of the business. The term charge safeguard then, at that point, is gotten from the idea that assuming an organization has more obligation, and hence utilizes a more prominent piece of its working benefits to pay for interest, those benefits are to some degree shielded from tax assessment.

Issues with Tax Shields

I have two objections to charge safeguards.

Right off the bat, having a circumstance where the organization you own has less benefit and calling it a safeguard appears to be somewhat insincere. What’s more second, while an organization may not pay charges on interest, the bank positively will. Premium pay is burdened, and frequently at a high rate. Thus, truly, what is happening is that the obligation regarding paying duties on a piece of an association’s benefit is being moved to its bank (an exchange, not a safeguard). Also one might ask how a bank should be made up for such an exchange?

This is a decent second to move to the loan specialist’s point of view, which is inconceivably significant in an LBO bargain. As you might have seen, the main word in LBO is utilized, and that is basically what’s genuinely going on with the game. While moneylenders come in all shapes and sizes, the loaning market overall does the occupation of valuing acknowledge hazard, with okay advances regularly having an expense at simply a little spread to the market’s without danger rate, and high-hazard credits having a lot higher rate, possibly in any event, including a value cooperation part or convertibility highlight which would permit the obligation to have value like returns.

Matched with the danger-based evaluating are hazard-based terms. What I mean by that will be that assuming a moneylender is giving a generally safe credit, they are probably going to have not many controls, no ensures, restricted detailing, and a lot of adaptability for the borrower. A similar bank giving a higher-hazard credit might require a wide range of ensures, agreements, and announcing. This checks out, as the higher-hazard moneylender will need extra affirmations and impetus arrangement from an organization’s proprietors and associates and will need to restrict the sorts of moves the organization can make just as recieve brief data about the organization’s monetary wellbeing.

These components, set up, can have wide ramifications for the reasonability of an LBO, thus the overlooked details are the main problem. An advance that pairs an organization’s obligation commitments yet in addition drastically builds the loan fee it pays on those commitments may not be accretive to the organization by any stretch of the imagination, charge safeguard be condemned. Also, an advance that has severe working pledges limiting interests in development or future acquisitions won’t work assuming the marketable strategy of the LBO exchange is to drive income development at the organization through add-on buys or weighty interests in natural development. The field-tested strategy and obligation plan need to cooperate, and a great deal of the accomplishment of an LBO exchange is predicated on knowing what the obligation market will bear and what it will acknowledge comparative with a particular chance as for valuing and terms.

Step by step instructions to Analyze an LBO Transaction

Changing gears from the overall ideas hidden LBOs, we should talk about the examination of a possible exchange according to a monetary viewpoint.

The investigation of an LBO is genuinely direct once you have a setup series of expectations for an organization’s current and future activities, it’s worth comparative with those tasks, and the expense of obligation—and other capital in the commercial center—for the exchange.

The objective of LBO investigation then, at that point, is to infer the possible worth of the organization’s value in a time of years past its procurement and to consolidate that worth gauge with whatever other money that can be conveyed by the organization en route (which by and large is restricted, as current money in an LBO is frequently either reinvested in the organization to drive development or used to reimburse obligation). When those numbers are determined, then, at that point, it’s genuinely easy to think of the extended complete pace of return utilizing our cherished bring measurements back: normally IRR, value different, or net benefit.

Diving into an extra degree of detail and zeroing in explicitly on the future worth of an organization’s value, the methodology that normally appears to be legit is to gauge the organization’s future pay (most frequently introduced as some rendition of EBITDA) and its worth various, generally introduced as the organization’s venture esteem/EBITDA and afterward to layer underwater capital expenses and reimbursements at that future chance to ascertain the future worth of its value. I utilize the expression “as a rule” here on the grounds that different methodologies, for example, limited income and other more fascinating methodologies—do exist, and also various products and worth drivers are at times utilized. In any case, for LBOs, EV/EBITDA less obligation is the methodology that I think most sensibly reflects possible acquisitions and is the most market-arranged methodology.

The Role of EBITDA

Given its commonness, we should talk about EBITDA in somewhat more detail. EBITDA is planned to be a sensible intermediary for how much pre-charge esteem the organization, overall, produces in a given timeframe.

How about we take every component autonomously to all the more likely comprehend the measurement. The measurement begins with income, which is the organization’s bookkeeping profit dependent on its continuous tasks. To begin with, premium expenses are added back to income since interest is a component of the organization’s absolute capitalization and not a “valid” cost of its tasks. The method for pondering this is that the organization creates a general benefit that can be shared by all gatherings that have a case on those benefits, including the two its moneylenders and its value financial backers. By picking various blends of obligation and value, you can move how those incomes are paid to various partners, however, the general measure of benefit won’t change, so interest cost is actually a decision that is made free of the organization’s functional achievement. It’s important for capital choice. Not tasks.

Then, charges are added back as they likewise can shift contingent upon capital construction and choices the organization makes about its activities, and surprisingly dependent on who the proprietors of an organization are and what its hierarchical design is. To put it plainly, checking out profit pre-charge and before interest permits a more steady evaluation of business tasks, in particular from the fairly elaborate reasoning fundamental its capitalization and its expense bill.

The initial two changes in accordance with arriving at EBITDA are genuinely clear, yet the contention for adapting to deterioration and amortization isn’t as straightforward. Deterioration and amortization are eliminated in light of the fact that they generally connect with recorded capital expenses of the organization and not to its continuous activities (or possibly not obviously).

For instance, envision an organization that purchases a retail property to work an apparel store. The organization creates again that is the contrast between the absolute deals of garments, the expense of those garments, and the functional costs it brings about to get those deals going (and to cover managerial overhead). Bookkeepers, nonetheless, will layer on an extra deterioration cost to show up at the organization’s income, contending that every year the business is inactivity it “wears out” part of its structure. Yet, this cost is bookkeeping fiction, and possibly completely separated from the real world. Imagine a scenario where the store has been opened in Manhattan during the 1980s. The land under the store may really have appreciated generously during the very time that the business was causing this “cost,” and may now be worth significantly more than the proprietor paid for it in any case. Then again, one can likewise envision the store having a sales register that may likewise be devalued. Here, the devaluation is more exact, as inside a time of years, the sales register may be supplanted and the worth of the current register by then may genuinely be zero. So it definitely should be viewed as a cost.

Changed EBITDA

These kinds of contentions frequently lead one down the way towards a changed EBITDA, which is sensible, yet all the same consistently doubtful. A wide range of expenses and components can be added or taken out regarding any organization to show up at its “valid” EBITDA. We should leave the deterioration connected with the sales register but overlook the devaluation connected with the structure. In any case, what might be said about the new store we’re opening down the road—should costs connected with that be remembered for EBITDA? It’s not actually connected with the current activity, and they are “once” costs. Also what might be said about the bonus made last year trading a novel, vintage thing at the store? Should that be remembered for EBITDA? What might be said about the proprietor’s child, who is utilized at the store yet is being paid double the market rate in compensation? Ought to there be a change for that? Isn’t that truly kind of a true proprietorship interest? The incline is dangerous and long, in any case, the directing light is to attempt to show up at a number that most decently mirrors the balanced-out benefit of the business in the long haul.

An incredible illustration of a discussion connected with changed EBITDA came in 2018 from WeWork. The collaborating business involved its own exclusive form of the measurement in its revelations for a security issue, where it imaginatively found much more additional items to develop its figures: “It deducted revenue, duties, devaluation, and amortization, yet additionally essential costs like promoting, general and authoritative, and advancement and configuration costs.” A financial backer hoping to put resources into the bond issue would have needed to think about the organization’s contention and choose if the changes were fitting or not, or to make their own estimation of the organization’s drawn-out benefit potential.

Venture Value

Venture esteem (EV) is the other significant piece of the worth estimation and mirrors the worth of the organization including its obligation, value, and other proprietorship claims on the organization, less any money held by the organization. The idea is that if EBITDA—or some changed adaptation of it—is the balanced out benefit of the organization and EV is its absolute worth and that there is some relationship that can be set up between them (EV/EBITDA). That difference would then be able to be a manual for the future worth of the organization or can be utilized as a benchmark for the worth of other, comparative organizations.

Presently, if as a financial backer we know the accompanying factors:

The value financing needed to finish the exchange

How much money do we hope to remove from it during the hold time frame as far as profits or buybacks, or through different means?

What the resource is relied upon to be worth toward the finish of our venture time period, by taking our future projection of EBITDA and increasing it by our best gauge of future EV/EBITDA

How much obligation will be owed at the hour of the exit

Every one of our own costs, as far as exchange and other holding costs.

Then, at that point, we will actually want to ascertain our net income. Furthermore from that point, we can apply our cherished return target (complete benefit, cash difference, IRR, NPV, or whatever we like) and choose if the exchange appears to be legit. Or if nothing else whether it’s a good idea for us.

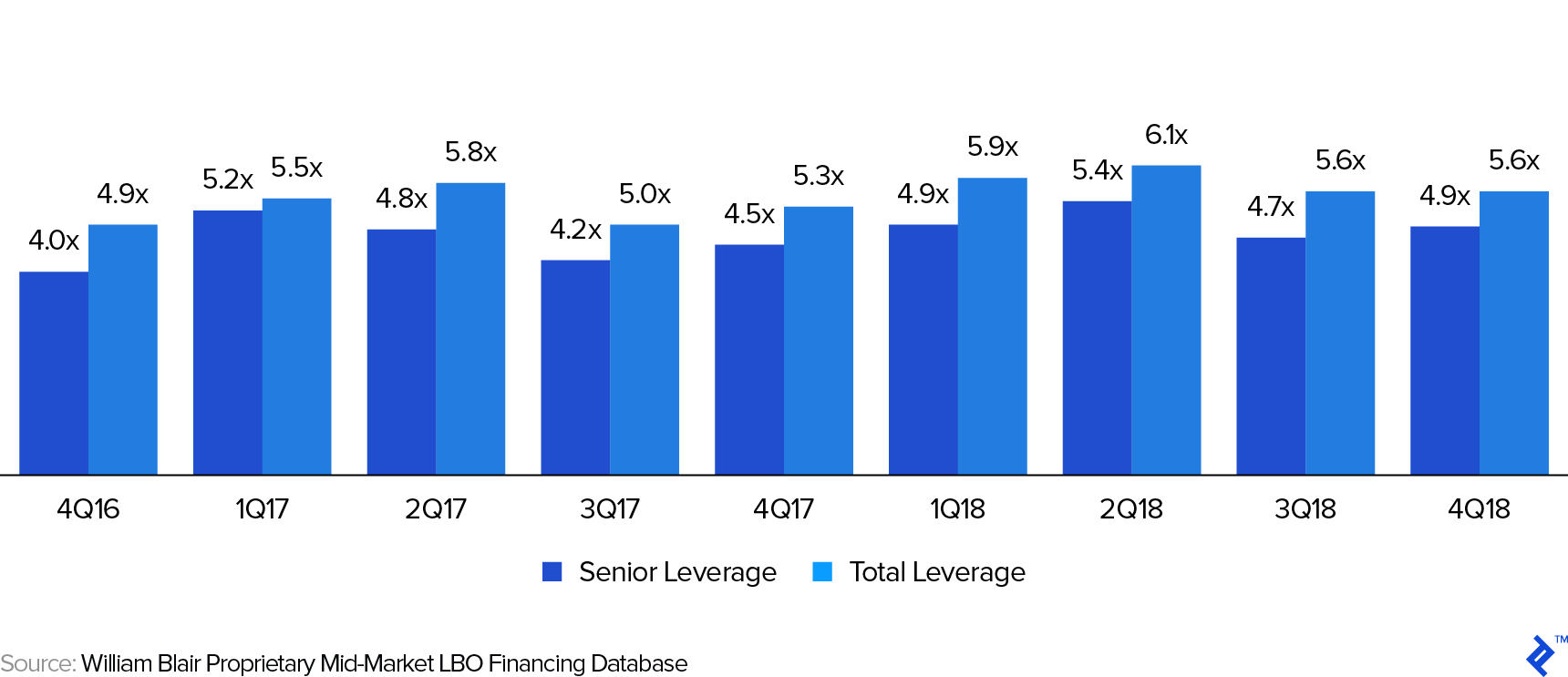

Influence Multiples: How Much Can Be Borrowed?

Getting back to EBITDA briefly, the other significant worth to EBITDA-based examination is that most banks working in the LBO space additionally view EBITDA as one of the key components connected with the sum they will loan against a business. Thusly, credits and their pledges are regularly cited dependent on EBITDA.

William Blair, a speculation bank, for instance, detailed mid-market EBITDA products for advances in the LBO area for the final quarter of 2018 at 5.6x on complete influence.

{kind=link}